More Articles

-

Slick TV ads often make financial planning and wealth management sound simple, but it’s usually not. Managing wealth requires knowing a lot about highly technical topics, like taxes, government regulations, and finance as well as history, psychology and how to communicate with loved ones about sensitive issues. This article highlights some of the knowledge needed to manage wealth and why it’s often so daunting without the help of an independent personal financial advisor who is familiar with your situation.

-

Understanding The Federal Reserve Mandate To End Inflation

The Federal Reserve System, the nation’s central bank, has a dual mandate to pursue maximum employment and maintain price stability. These two priorities are currently treated equally, but that was not always the case. In fact, the Fed’s bias toward maximizing employment was a critical driver of the stagflation that plagued the U.S. in the late 1960s and 1970s. Recognizing the need to balance price stability and maximum employment, in 1977, Congress revised the Federal Reserve Act.

-

Fed Governor Kugler Details Inflation And Economic Outlook

The 12-month inflation rate, as measured by the personal consumption expenditures (PCE) index, was 2.6% in December, down from its peak of 7.1% in June 2022, and the six-month rate for PCE inflation was even lower, at 2%, which is the target rate set by the Federal Reserve.

-

Why Rates May Not Be Cut Until June

The cost of a loan to buy a home, car, college education, and achieve the American Dream is staying the same for now. As expected, Federal Reserve Chairman Jerome Powell said the central bank did not lower loan rates following the Fed’s Wednesday, Jan. 31, 2024, policy meeting.

-

Practical Suggestions For Achieving Your 2024 Resolutions

New Year’s resolutions usually fail because they‘re often too hard to achieve. After six months, only 10% of people who make resolutions achieve them or remain committed to them, , according to a study by Dr. Mark Griffiths, a Chartered Psychologist and Distinguished Professor of Behavioral Addiction at the Nottingham Trent University. What can you do to make financial, medical, or other personal resolutions more likely to be achieved?

-

A Sign Of Progress In Solving U.S. Economic Problems

The Federal Reserve appears to be pulling off a feat most experts did not believe it could: ending its aggressive inflation-fighting campaign of 11 interest rate hikes without tipping the U.S. economy into a recession.

-

Fed Keeps Rates Unchanged; Expects Easing In 2024

To promote transparency and free markets, the Federal Reserve System began publishing the opinions of the 19 U.S. central bankers that decide interest rate policy.

-

Have You Logged Into Your Social Security Account?

Have you logged in to your Social Security account? Creating an online account at SSA.gov is an important first step in understanding your retirement income situation. However, only about 60 million of the 160 million individuals in the U.S. labor force who have Social Security accounts have created a way to access the Social Security Administration’s website.

-

The Great Fake Out Of 2023 Is Poised To Extend Into 2024

All year long, the economy and stock prices have fooled experts and consumers, outperforming expectations month after month.

-

Test Your Financial Planning IQ

The five questions below are a challenge meant to allow you to assess your knowledge of investing, tax and financial planning. If you have been following our news stream, this quiz draws on familiar ground. The answers are below.

- Read More

Planning Briefs

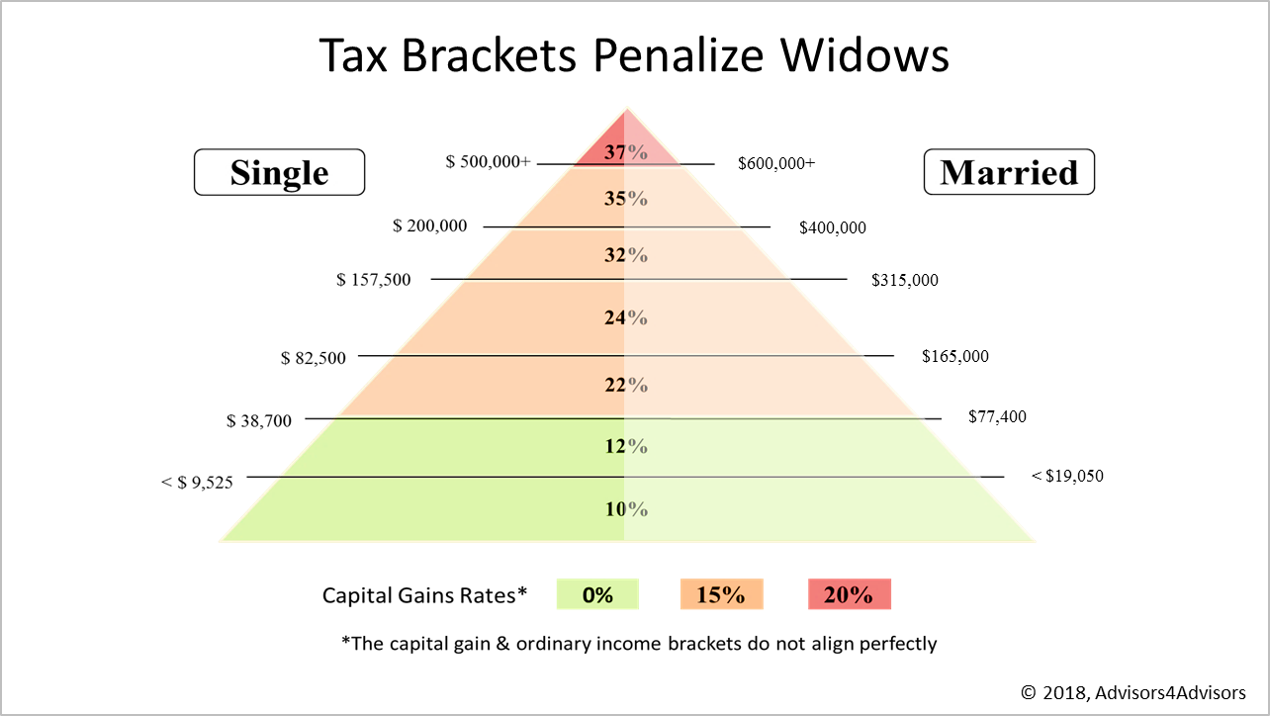

Reduce Your Widow's Tax Bill Materially Annually

Published Monday, July 30, 2018 at: 7:00 AM EDT

This is a good time to consider converting a traditional individual retirement account into a Roth IRA. Tax rates are low but unlikely to stay that way. Here's a long-term strategy that takes advantage of the current tax policy and economic fundamentals - a tax-efficient retirement investment and avoids a new twist in the Tax Cut And Jobs Act that penalizes widows.

The Rules. With a traditional individual retirement account (IRA), taxes on gains reinvested are deferred. An IRA grows with no taxes owed. When you retire, withdrawals are taxed as income. A Roth IRA is different. You pay income tax upfront and Uncle Sam promises tax-free withdrawals when you're retired.

The Math. According to data from the non-partisan Congressional Budget Office, math will drive a surge in the $21 trillion U.S. debt starting in 2023, when interest owed on the debt accelerates, as does the risk of default. As 2023 nears, running trillion-dollar budget deficits annually becomes an increasingly untenable policy and tax rates are likely to rise.

Inflation, too. Inflation has been low for many years. While it is not expected to rise sharply, the real cost of the federal debt would be reduced if inflation rises. Inflation is unlikely to work against those converting to a Roth IRA in 2018.

Widow Penalty. Many surviving spouses will face a tax penalty after losing a mate under the new tax brackets enacted by the Tax Cuts And Jobs Act. For example, a couple with $170,000 of adjusted gross income is in the 24% top bracket, but after one spouse dies, the survivor would fall into the 32% bracket.

Avoiding The Widow Penalty. Retired married couples converting from a traditional IRA to a Roth account can avert the widow penalty with proper planning. Since Roth accounts generate tax-free income, converting to a Roth places a surviving spouse in a lower tax bracket. For example, a couple with $170,000 of adjusted gross income (AGI) would convert from a traditional IRA to a Roth IRA, lowering their AGI to less than $157,500. If one spouse dies, the survivor would be in the 24% bracket applied to singles with up to $157,500 of adjusted gross income.

Not For Everyone. Converting makes no sense unless you have cash on hand to pay the income tax on withdrawals from your traditional IRA. Paying taxes owed on a conversion by withdrawing larger amounts from a traditional IRA usually limits a nest egg's growth potential and is unwise.

Tax-sensitive investing is complicated, and this simplified version of the rules and examples are only intended to encourage to plan properly because a move like this can reduce a tax bill materially and annually for a widow.

We evaluate tax planning opportunities for clients. Please contact our office to talk about your personal situation or if you have any questions about this strategy.

© 2024 Advisor Products Inc. All Rights Reserved.