More Articles

-

Slick TV ads often make financial planning and wealth management sound simple, but it’s usually not. Managing wealth requires knowing a lot about highly technical topics, like taxes, government regulations, and finance as well as history, psychology and how to communicate with loved ones about sensitive issues. This article highlights some of the knowledge needed to manage wealth and why it’s often so daunting without the help of an independent personal financial advisor who is familiar with your situation.

-

Understanding The Federal Reserve Mandate To End Inflation

The Federal Reserve System, the nation’s central bank, has a dual mandate to pursue maximum employment and maintain price stability. These two priorities are currently treated equally, but that was not always the case. In fact, the Fed’s bias toward maximizing employment was a critical driver of the stagflation that plagued the U.S. in the late 1960s and 1970s. Recognizing the need to balance price stability and maximum employment, in 1977, Congress revised the Federal Reserve Act.

-

Fed Governor Kugler Details Inflation And Economic Outlook

The 12-month inflation rate, as measured by the personal consumption expenditures (PCE) index, was 2.6% in December, down from its peak of 7.1% in June 2022, and the six-month rate for PCE inflation was even lower, at 2%, which is the target rate set by the Federal Reserve.

-

Why Rates May Not Be Cut Until June

The cost of a loan to buy a home, car, college education, and achieve the American Dream is staying the same for now. As expected, Federal Reserve Chairman Jerome Powell said the central bank did not lower loan rates following the Fed’s Wednesday, Jan. 31, 2024, policy meeting.

-

Practical Suggestions For Achieving Your 2024 Resolutions

New Year’s resolutions usually fail because they‘re often too hard to achieve. After six months, only 10% of people who make resolutions achieve them or remain committed to them, , according to a study by Dr. Mark Griffiths, a Chartered Psychologist and Distinguished Professor of Behavioral Addiction at the Nottingham Trent University. What can you do to make financial, medical, or other personal resolutions more likely to be achieved?

-

A Sign Of Progress In Solving U.S. Economic Problems

The Federal Reserve appears to be pulling off a feat most experts did not believe it could: ending its aggressive inflation-fighting campaign of 11 interest rate hikes without tipping the U.S. economy into a recession.

-

Fed Keeps Rates Unchanged; Expects Easing In 2024

To promote transparency and free markets, the Federal Reserve System began publishing the opinions of the 19 U.S. central bankers that decide interest rate policy.

-

Have You Logged Into Your Social Security Account?

Have you logged in to your Social Security account? Creating an online account at SSA.gov is an important first step in understanding your retirement income situation. However, only about 60 million of the 160 million individuals in the U.S. labor force who have Social Security accounts have created a way to access the Social Security Administration’s website.

-

The Great Fake Out Of 2023 Is Poised To Extend Into 2024

All year long, the economy and stock prices have fooled experts and consumers, outperforming expectations month after month.

-

Test Your Financial Planning IQ

The five questions below are a challenge meant to allow you to assess your knowledge of investing, tax and financial planning. If you have been following our news stream, this quiz draws on familiar ground. The answers are below.

- Read More

Planning Briefs

When Will Post-Covid Financial Pain Stop?

Published Thursday, October 13, 2022 at: 7:06 PM EDT

The Standard & Poor’s 500 stock index fell into a bear market on June 13, 2022, rebounded in the summer, and then tanked again as summer ended; autumn is beginning with the fall continuing. This morning’s higher than expected inflation number may make you wonder when the post-Covid financial pain will stop.

Using history as a guide, the bad news is probably not all behind us but it’s also not so far from ending, according to financial historian Mark J. Higgins.

In a two-hour course for financial professionals, Mr. Higgins, says the post-Covid financial challenges facing the U.S. are a lot like the post-pandemic years following The Great Influenza of 1918 and World War I.

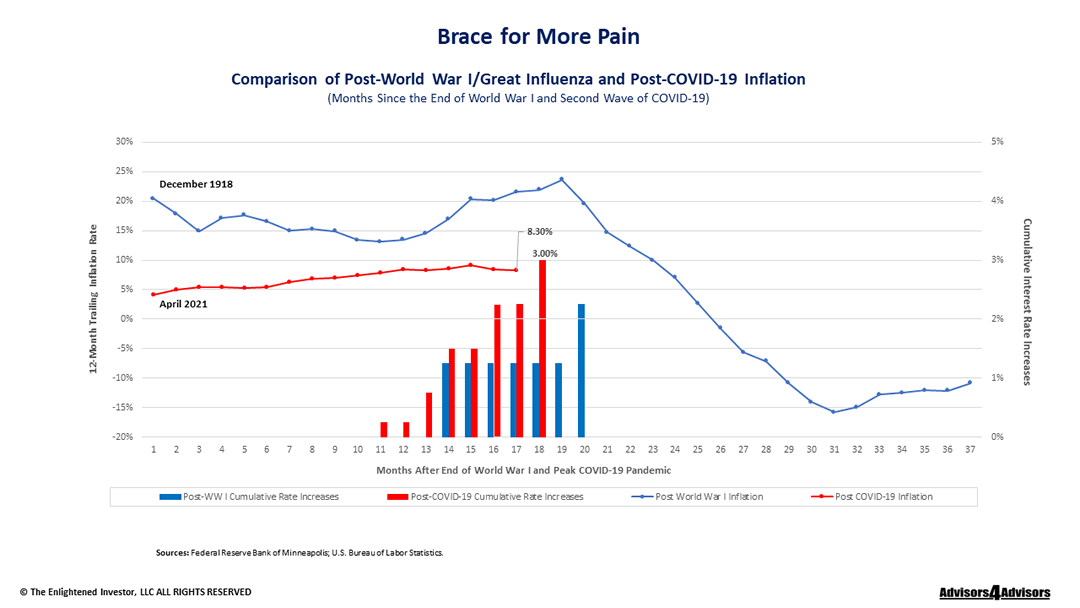

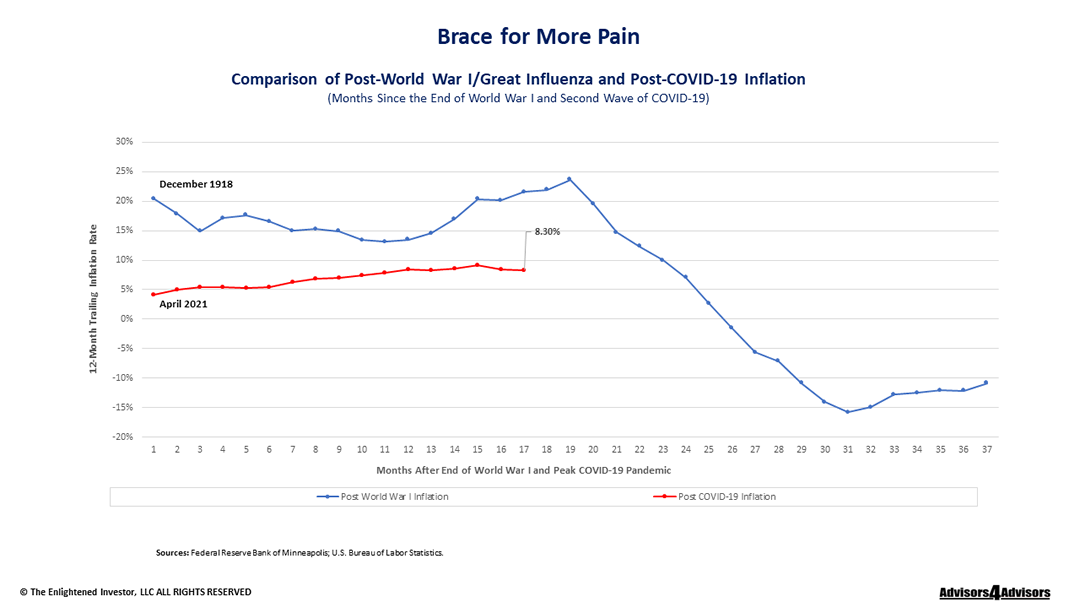

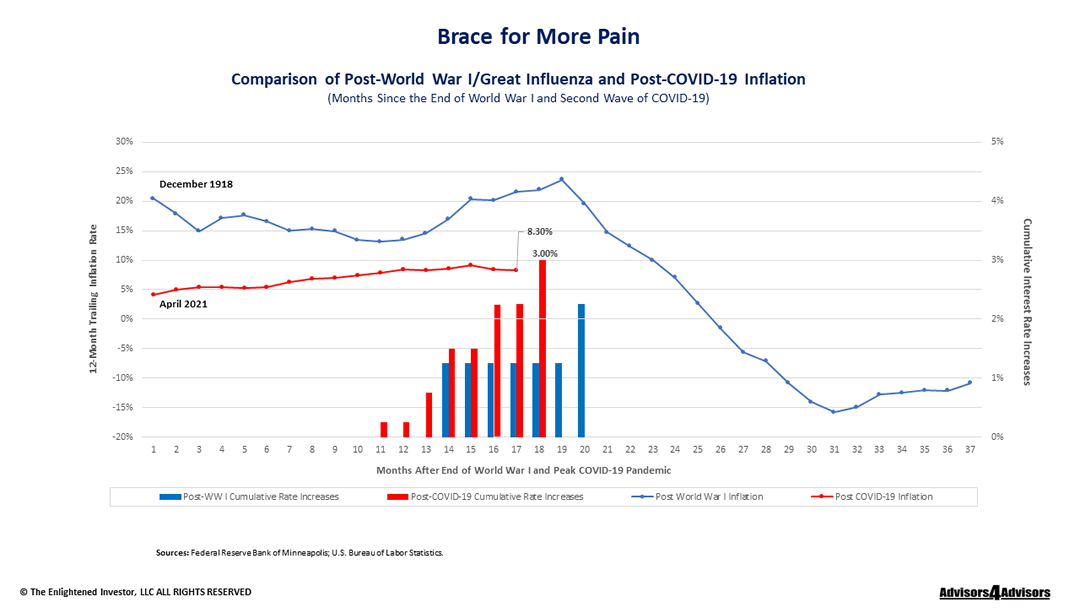

To illustrate the point, the blue line in this chart shows the trailing 12-month inflation rate for the 37 months after the peak of The Great Influenza, and the red line shows the trailing 12-month inflation rate for the 17 months since the end of the COVID-19 peak period of quarantine in April 2021.

Twenty months after the peak in the Spanish flu, Fed tightening finally broke the back of the inflation cycle, throwing the economy into a recession.

The red line, representing the annual inflation rate in today’s post-Covid world, is approaching the pivotal 20-month mark of the post-pandemic inflation crisis a century ago.

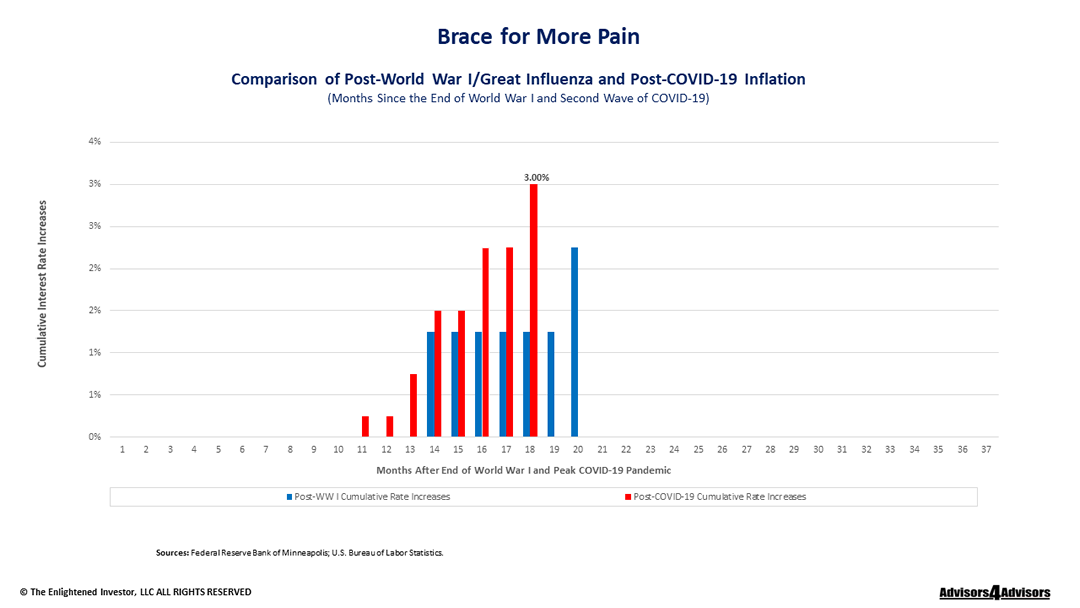

Meanwhile, the blue bars show the cumulative interest rate increases by the Federal Reserve after the 1918 pandemic and the red bars show the Fed’s actions so far in the post Covid-19 era through today. “We are right about at the point when disinflation starts and the economy enters recession,” says Mr. Higgins.

So, what does this historical parallel mean to investors?

It means investors should expect:

1. more rate hikes by the Fed to destroy demand for goods and services before inflation is tamed. Prepare for jobs to be harder to find, new-home building to continue to slow, slower earnings growth on the blue-chip companies in the S&P 500, and continued trouble in the stock market.

2. waves of panic-driven stock selling by investors no longer able to resist dumping stocks, as losses mount beyond -25%, -30% or -35% from the all time high at the start of 2022.

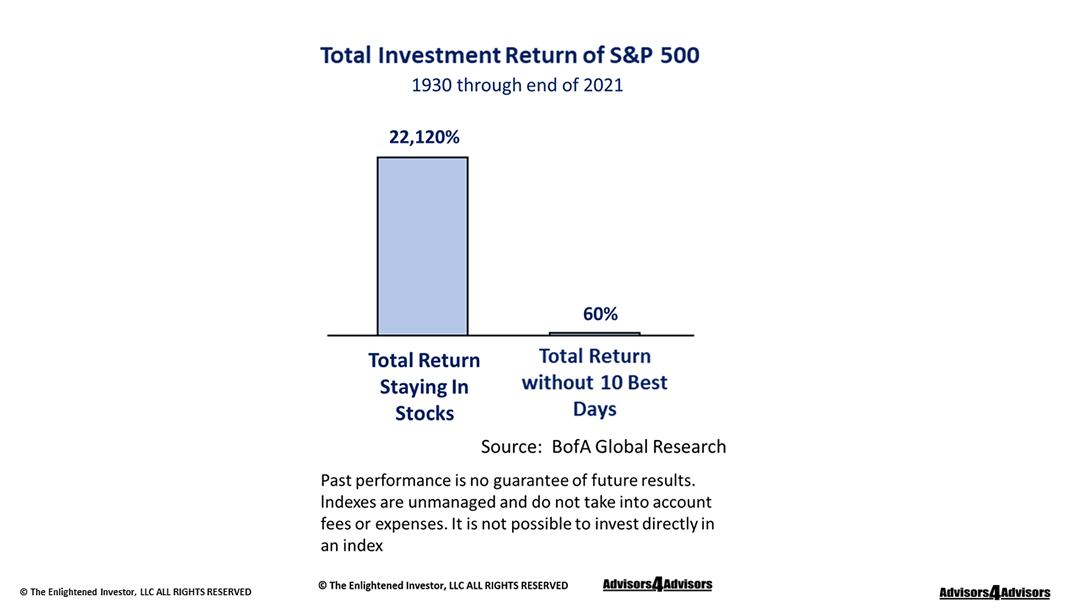

Keep in mind, says Mr. Higgins, studies have shown timing when to sell and buy stocks is too hard to do consistently with reliability. He cites a 2022 study by BofA Global Securities that showed missing the just 10 best days of every decade since the 1930s would have resulted in a +22,120% total return for an investor who did not sell through the end of 2001. In comparison, missing the 10 best days of every decade in the same period resulted in a relatively paltry +60% total return, which demonstrates the futility of trying to get in and out of stocks at just the right moment.

Mark J. Higgins is a regular contributor to our articles. His book, “Becoming an Enlightened Investor,” a full financial history of the United States, is expected to be available on Amazon in March 2023.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances. The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions. This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice.

©2022 Advisor Products Inc. All Rights Reserved.