More Articles

-

Slick TV ads often make financial planning and wealth management sound simple, but it’s usually not. Managing wealth requires knowing a lot about highly technical topics, like taxes, government regulations, and finance as well as history, psychology and how to communicate with loved ones about sensitive issues. This article highlights some of the knowledge needed to manage wealth and why it’s often so daunting without the help of an independent personal financial advisor who is familiar with your situation.

-

Understanding The Federal Reserve Mandate To End Inflation

The Federal Reserve System, the nation’s central bank, has a dual mandate to pursue maximum employment and maintain price stability. These two priorities are currently treated equally, but that was not always the case. In fact, the Fed’s bias toward maximizing employment was a critical driver of the stagflation that plagued the U.S. in the late 1960s and 1970s. Recognizing the need to balance price stability and maximum employment, in 1977, Congress revised the Federal Reserve Act.

-

Fed Governor Kugler Details Inflation And Economic Outlook

The 12-month inflation rate, as measured by the personal consumption expenditures (PCE) index, was 2.6% in December, down from its peak of 7.1% in June 2022, and the six-month rate for PCE inflation was even lower, at 2%, which is the target rate set by the Federal Reserve.

-

Why Rates May Not Be Cut Until June

The cost of a loan to buy a home, car, college education, and achieve the American Dream is staying the same for now. As expected, Federal Reserve Chairman Jerome Powell said the central bank did not lower loan rates following the Fed’s Wednesday, Jan. 31, 2024, policy meeting.

-

Practical Suggestions For Achieving Your 2024 Resolutions

New Year’s resolutions usually fail because they‘re often too hard to achieve. After six months, only 10% of people who make resolutions achieve them or remain committed to them, , according to a study by Dr. Mark Griffiths, a Chartered Psychologist and Distinguished Professor of Behavioral Addiction at the Nottingham Trent University. What can you do to make financial, medical, or other personal resolutions more likely to be achieved?

-

A Sign Of Progress In Solving U.S. Economic Problems

The Federal Reserve appears to be pulling off a feat most experts did not believe it could: ending its aggressive inflation-fighting campaign of 11 interest rate hikes without tipping the U.S. economy into a recession.

-

Fed Keeps Rates Unchanged; Expects Easing In 2024

To promote transparency and free markets, the Federal Reserve System began publishing the opinions of the 19 U.S. central bankers that decide interest rate policy.

-

Have You Logged Into Your Social Security Account?

Have you logged in to your Social Security account? Creating an online account at SSA.gov is an important first step in understanding your retirement income situation. However, only about 60 million of the 160 million individuals in the U.S. labor force who have Social Security accounts have created a way to access the Social Security Administration’s website.

-

The Great Fake Out Of 2023 Is Poised To Extend Into 2024

All year long, the economy and stock prices have fooled experts and consumers, outperforming expectations month after month.

-

Test Your Financial Planning IQ

The five questions below are a challenge meant to allow you to assess your knowledge of investing, tax and financial planning. If you have been following our news stream, this quiz draws on familiar ground. The answers are below.

- Read More

Planning Briefs

Retirement Income Portfolio Survival

Published Wednesday, February 6, 2019 at: 7:00 AM EST

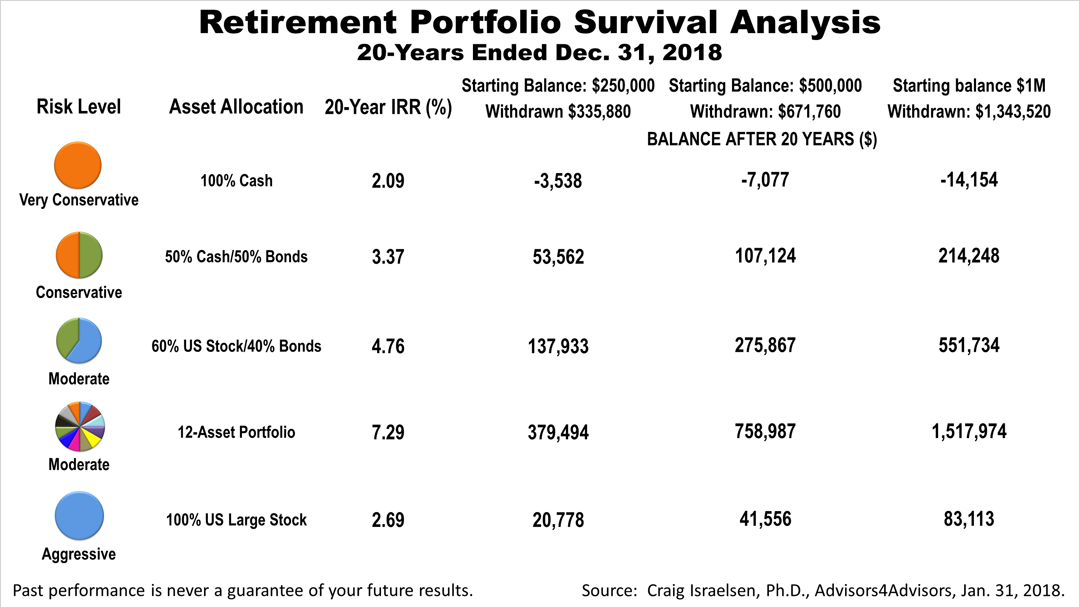

As financial professionals, we believe understanding the dynamics of retirement income portfolio risk can be crucial to investment success. The survivability of five hypothetical retirement portfolios over the 20-year period ended December 31st, 2018 shown in the accompanying table is not intended as investment advice but is intended to help clients better understand retirement portfolio risk and conquer perhaps the worst of all financial fears: running out of money in retirement. The data is based on a continuing professional education session by Professor Dr. Craig Israelsen, an independent economist whose research we license.

The results of the five portfolio risk levels illustrated a range from very conservative to aggressive. All five portfolios assume a retiree withdrew 5% of the portfolio value annually, and annually increased withdrawals by 3% to keep up with inflation. Pick whichever starting balance — $250,000, $500,000 or $1 million — best applies to your situation.

What stands out is that the most diversified of the five portfolios outperformed considerably — broad diversification worked! That diversification worked may come as no great surprise; conventional wisdom and academic research hold that diversifying is wise. Remarkably, diversification worked even though this was a 20-year period of low returns on stocks.

Stocks, a riskier investment in a retirement portfolio, showed an internal rate of return over the 20 years of just 2.69% — only six-tenths of 1% better than the least risky of the five portfolios, the one 100% invested in short-term Treasury Bills.

Why did stocks perform so poorly? The 20-year period started in 1999, at the peak of the dot-com bubble. The Standard Poor's 500 index did not recover until 2006, and then it dropped again in the bear market of 2008. A retiree picked a terrible 20 years to be an aggressive investor 100% invested in stocks.

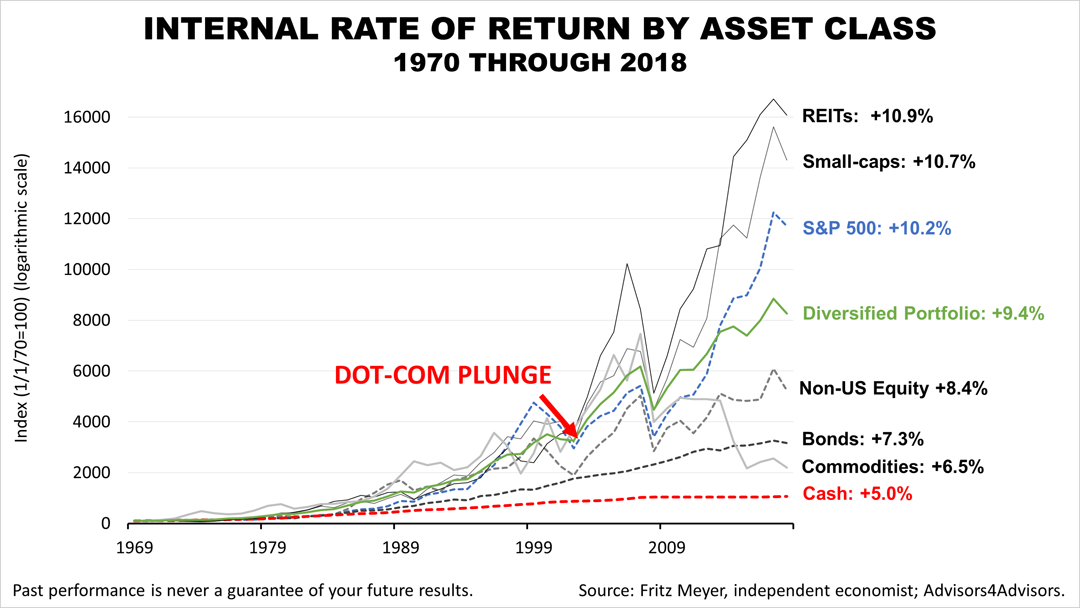

Over the much longer 49-year period, stocks did outperform cash by a huge amount and they also outperformed a diversified portfolio.

The point is that even in this terrible period for stocks, the growth engine of a retirement portfolio, a broadly diversified portfolio outperformed. The next 20 years are likely to be as unpredictable as the last 20 years, but this illustrates how broad diversification helped a retirement portfolio survive through a period in which stocks performed unexpectedly poorly.

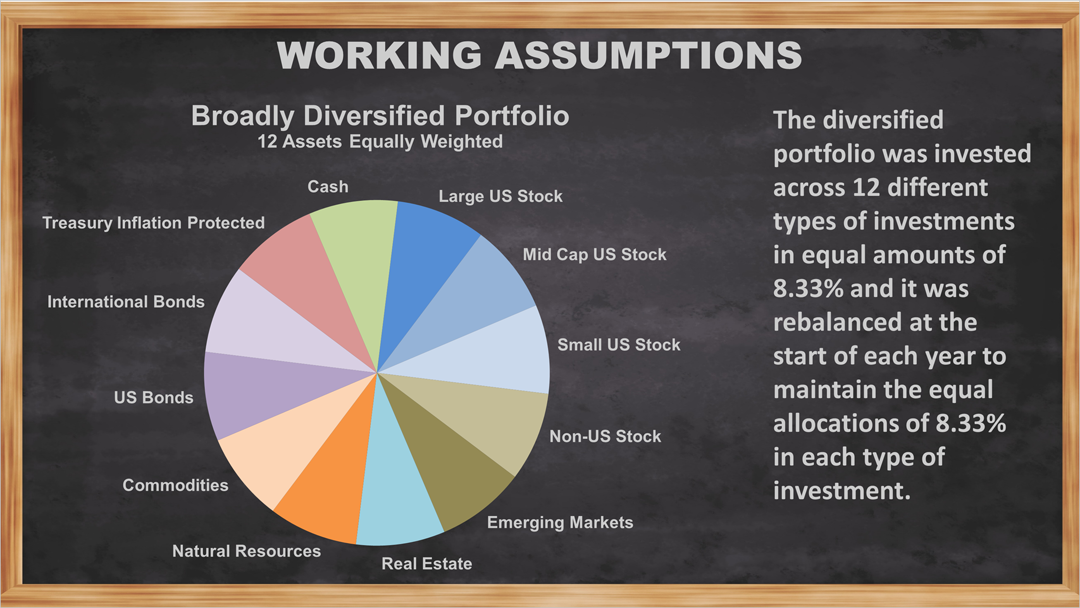

These are the indexes that represent the ETFs used in the Passive 7Twelve® Portfolio.

© 2024 Advisor Products Inc. All Rights Reserved.