More Articles

-

Slick TV ads often make financial planning and wealth management sound simple, but it’s usually not. Managing wealth requires knowing a lot about highly technical topics, like taxes, government regulations, and finance as well as history, psychology and how to communicate with loved ones about sensitive issues. This article highlights some of the knowledge needed to manage wealth and why it’s often so daunting without the help of an independent personal financial advisor who is familiar with your situation.

-

Understanding The Federal Reserve Mandate To End Inflation

The Federal Reserve System, the nation’s central bank, has a dual mandate to pursue maximum employment and maintain price stability. These two priorities are currently treated equally, but that was not always the case. In fact, the Fed’s bias toward maximizing employment was a critical driver of the stagflation that plagued the U.S. in the late 1960s and 1970s. Recognizing the need to balance price stability and maximum employment, in 1977, Congress revised the Federal Reserve Act.

-

Fed Governor Kugler Details Inflation And Economic Outlook

The 12-month inflation rate, as measured by the personal consumption expenditures (PCE) index, was 2.6% in December, down from its peak of 7.1% in June 2022, and the six-month rate for PCE inflation was even lower, at 2%, which is the target rate set by the Federal Reserve.

-

Why Rates May Not Be Cut Until June

The cost of a loan to buy a home, car, college education, and achieve the American Dream is staying the same for now. As expected, Federal Reserve Chairman Jerome Powell said the central bank did not lower loan rates following the Fed’s Wednesday, Jan. 31, 2024, policy meeting.

-

Practical Suggestions For Achieving Your 2024 Resolutions

New Year’s resolutions usually fail because they‘re often too hard to achieve. After six months, only 10% of people who make resolutions achieve them or remain committed to them, , according to a study by Dr. Mark Griffiths, a Chartered Psychologist and Distinguished Professor of Behavioral Addiction at the Nottingham Trent University. What can you do to make financial, medical, or other personal resolutions more likely to be achieved?

-

A Sign Of Progress In Solving U.S. Economic Problems

The Federal Reserve appears to be pulling off a feat most experts did not believe it could: ending its aggressive inflation-fighting campaign of 11 interest rate hikes without tipping the U.S. economy into a recession.

-

Fed Keeps Rates Unchanged; Expects Easing In 2024

To promote transparency and free markets, the Federal Reserve System began publishing the opinions of the 19 U.S. central bankers that decide interest rate policy.

-

Have You Logged Into Your Social Security Account?

Have you logged in to your Social Security account? Creating an online account at SSA.gov is an important first step in understanding your retirement income situation. However, only about 60 million of the 160 million individuals in the U.S. labor force who have Social Security accounts have created a way to access the Social Security Administration’s website.

-

The Great Fake Out Of 2023 Is Poised To Extend Into 2024

All year long, the economy and stock prices have fooled experts and consumers, outperforming expectations month after month.

-

Test Your Financial Planning IQ

The five questions below are a challenge meant to allow you to assess your knowledge of investing, tax and financial planning. If you have been following our news stream, this quiz draws on familiar ground. The answers are below.

- Read More

Planning Briefs

Financial Planning For The Long Run Amid The COVID-19 Epidemic

Published Tuesday, April 14, 2020, 8 p.m. EST

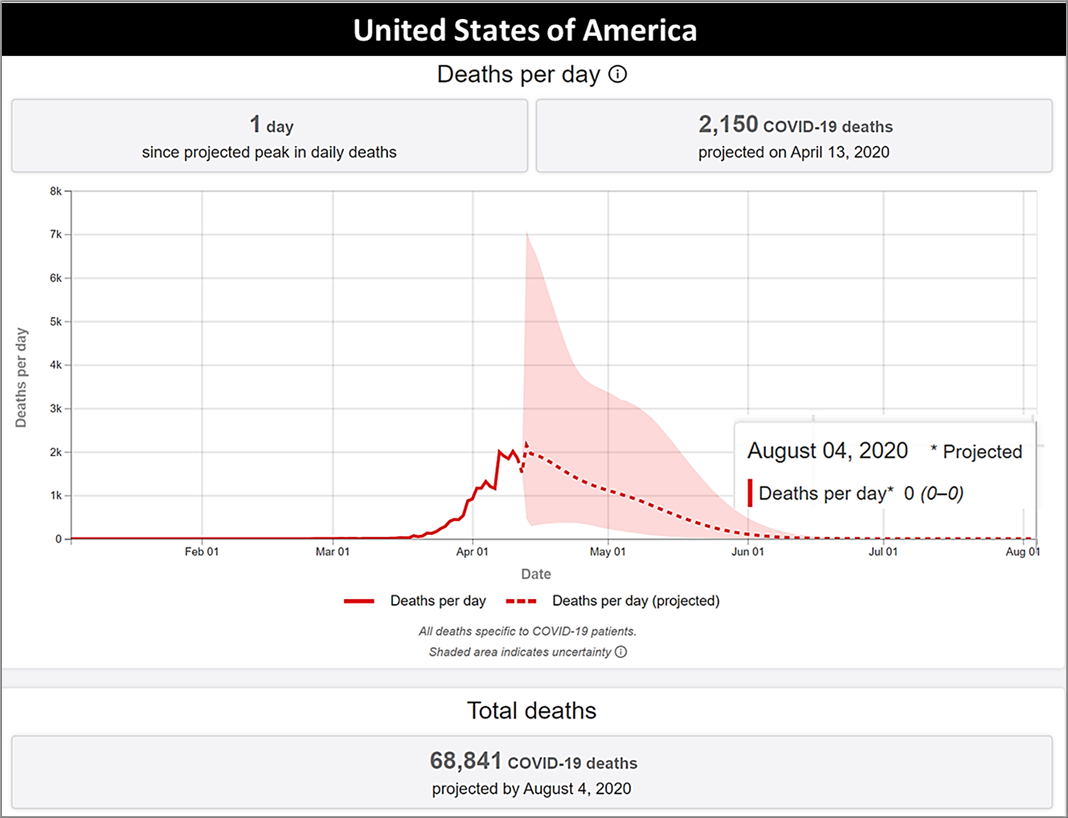

- By August 4, 2020, the Institute of Health Metrics and Evaluation (IHME), an independent public health research center at the University of Washington, expected 68,841 deaths from COVID-19 in the U.S. IHME's April 13 statistical model, if accurate, would exceed the 58,209 Americans killed in the 14-year Vietnam War. and the 54,246 American lives lost in the three-year Korean War. The human toll in sickness, suffering, and grief is unimaginable.

Almost overnight, the crisis has changed the financial and economic outlook. Change like this is frightening and brings new risks, but it also brings new opportunities. Here's a short list of what to do now.

Do Not Despair. As grim as things are, the models forecast an end to the epidemic. It's not a permanent condition. It will end. IHME, which is funded by the Bill and Melinda Gates' foundation, may turn out to be imprecise about the exact date of the end of COVID-19 deaths, and a second wave of the virus is a risk. Life may not be quite the same, for at least a couple of years and possibly longer, but life goes on. A survivor of the 1918 Spanish flu epidemic, according to The Wall Street Journal, said it took a couple of years before social, and, in turn, economic conditions returned to normalcy.

Stocks. The Standard & Poor's 500 lost about a one-third of its value from an all-time closing high on February 19 through the ultimate low on March 23 and it then has subsequently rebounded 25% off its low. Lower stock valuations may present a unique tax and financial planning opportunity. For example, if you own securities with large losses in a taxable portion of your portfolio, you might consider selling those assets at a loss. This concept is known as tax-loss harvesting. Losses on assets held for more than one year can be used to offset capital gains realized on other assets. So long as you do not buy securities that are identical or substantially the same, you can buy a similar asset to match your portfolio's risk level. The replacement asset will then have a lower cost-basis and more of your investment will ultimately be subject to favorable long-term capital tax treatment.

Roth IRA Conversions. Lower stock values make present an opportunity to convert some portion, or all, of a traditional IRA to a Roth IRA. Traditional IRAs are taxed as ordinary income upon withdrawal, while Roth IRAs are always tax free upon withdrawal. However, when you convert any portion of a traditional IRA to a tax-free Roth account, you must pay tax on the withdrawn amount at your current income tax rate. With asset values having been lowered by the bear market, the taxes owed on assets you wish to convert are commensurately lower, making the cost of converting to a tax-free Roth account less costly and lowering your tax bracket in the years ahead on withdrawals from the Roth IRA.

Paycheck Protection Program (PPP). On Friday, March 27, 2020, the Coronavirus Aid Relief Economic Security Act, a history-making $2.2 trillion stimulus law, allocating $349 billion in loans to business owners in need, and the loans are to be forgiven if you spend the money within the proscribed eight- week time frame to retain your employees. PPP is the primary relief program sponsored by the U.S. Government to aid business owners. PPP is expected to distribute its $349 billion by late April. Additional funding from Congress is widely expected, but it should be noted that the forgivable loans are distributed on a first-come, first-served basis. With 30 million small businesses, this is the one thing business owners want to get right. Contact us if you have questions about how to proceed.

Paycheck Protection Program (PPP). On Friday, March 27, 2020, the Coronavirus Aid Relief Economic Security Act, a history-making $2.2 trillion stimulus law, allocating $349 billion in loans to business owners in need, and the loans are to be forgiven if you spend the money within the proscribed eight- week time frame to retain your employees. PPP is the primary relief program sponsored by the U.S. Government to aid business owners. PPP is expected to distribute its $349 billion by late April. Additional funding from Congress is widely expected, but it should be noted that the forgivable loans are distributed on a first-come, first-served basis. With 30 million small businesses, this is the one thing business owners want to get right. Contact us if you have questions about how to proceed.

Wealth Transfers. For individuals with taxable estates, unprecedented low interest rates make it smart to consider the use of specially-designed trusts, such as a:

- Grantor Retained Annuity Trust (GRAT)

- Intentionally Defective Grantor Trust (IDGT)

- Generation Skipping Trust (GST)

Estates Currently In Administration. If you are a beneficiary of an estate in the administrative process of distributing assets, the change in asset values may have created a tax-loss harvesting opportunity. In addition, the lower asset values make it prudent for spousal beneficiaries of a qualified retirement account under administration to evaluate a partial or complete disclaimer of inherited assets.

Stay In Touch. The strategic opportunities for individuals described above do not necessarily contemplate your unique personal situation. If you have a specific question about any of this, or how it may apply to you, please contact us.

Nothing contained herein is to be considered a solicitation or research material. It is subject to change without notice. Strategies referenced herein do not take into account your personal objectives, financial situation or particular needs of any specific person. The material represents an assessment of financial, economic and tax law at a specific point in time. The sources are thought to be reliable but could be wrong about important facts.

The U.S. Government's response to the Coronavirus crisis implements new regulations and their precise impact may not be available at the time this was written or could be subject to change by U.S. Government agencies, such as the SBA.

© 2024 Advisor Products Inc. All Rights Reserved.